In an era characterized by digital transformation and lightning-fast transactions, the persistence of paper checks feels like a frustrating anachronism, almost as if you are stepping into a time warp where efficiency and technology don't exist - "Welcome to the 21st century, where we still act like it's the 19th."

For accounts receivable teams, these antiquated payment methods have become more of a hindrance than a convenience. As businesses strive for efficiency, accuracy, and streamlined processes, the cumbersome nature of paper checks stands out as a major obstacle. From delays in processing to increased manual labor and the heightened risk of errors, the continued reliance on paper checks is casting a shadow over the productivity and effectiveness of modern accounts receivable operations.

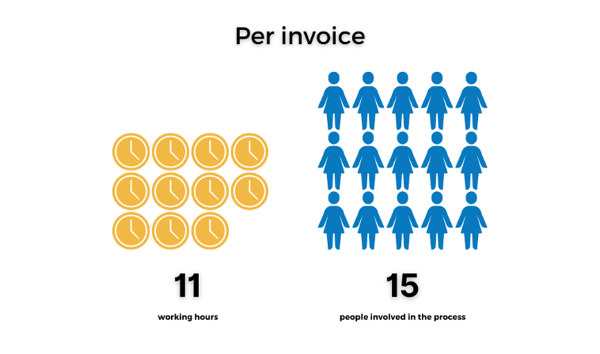

It’s a time-consuming process

Dealing with the receipt and processing of checks is a manual operation. In fact, senior AR decision makers estimate that, on average, 11 working hours are spent managing a single invoice, with 78% reporting that up to 15 people are involved in this process! It’s because an AR team dealing with paper check payments need to take scans of all the checks and remittances, where each check needs to be physically scanned or photocopied for record-keeping purposes. Similarly, manually extracting payment and remittance information from check stubs further adds to the processing time. The extracted data then needs to be manually entered into the enterprise resource planning (ERP) system or accounting software. Manual matching of remittances to respective invoices and posting them into the ERP system can be a time-intensive task, especially when dealing with a large volume of checks. These manual processes collectively prolong the payment cycle, resulting in increased Days Sales Outstanding (DSO) and impacting cash flow. It’s no wonder that on average, manual processing of payments is 67% more time-consuming compared to automated payment solutions.

Furthermore, this manual process mandates employees to be physically present at the office to process, where unforeseen circumstances such as illnesses or even vacations can cause setbacks in check and payment processing (especially when you need 15 people for a single invoice!)

Increased operational costs

The costs associated with processing paper checks are significantly higher compared to digital payment methods. It is estimated that the manual processing costs for US payments are in the range of $12-$30 per invoice, whereas on an annual basis, paper invoice processing can cost over $170K.

Banks often charge fees for services related to check processing, such as lockbox services. These fees can vary based on factors such as the volume of checks and the complexity of the processing requirements. Additionally, manual processes involved in handling checks, such as manual data entry, verification, and reconciliation, require significant manpower and time, which contributes to increased labor costs.

Limited payment tracking and visibility

Imagine trying to keep track of the status of hundreds of paper checks and their payment information. The manual nature of the process makes it difficult to determine the precise timestamp when a check is processed, cashed, and updated in the bank database. As a result, businesses may lack real-time visibility into the payment statuses, leading to uncertainty and potential delays in updating their accounts receivable records.

Lost or bounced checks can further complicate the visibility, causing late payments and potentially damaging customer relationships. The lack of insights into a business’s cash flow can be challenging for accounts receivable teams to prioritize and handle payment disputes efficiently, as they may not have a clear picture of the cash inflows and outflows.

Risk of errors

63% of firms with highly automated AR processes experience fewer invoicing errors, according to a study by PYMNTs.com. Why? Because of the manual handling and data extraction from paper checks, the likelihood of inaccuracies and discrepancies is increased and inevitable. By performing the manual key-in for capturing remittance information, human errors in data entry can occur, leading to incorrect payment details. Gathering remittance information from different sources, such as emails and web portals, further adds to the complexity and potential for mistakes.

Incorrectly recorded payment details or mismatched remittance data can result in payment disputes or deductions that require significant manual effort, such as calculating line items, communicating with customers, and resolving discrepancies.

Fraud and security risks

Sixty-three percent of respondents report that their organizations faced fraudulent activity via checks. Three-fourths of organizations currently using checks do not plan to discontinue issuing checks, according to the 2023 AFP® Payments Fraud and Control Survey Report. Paper checks pose significant risks in terms of fraud and security breaches, with can include counterfeit checks and forged signatures. Additionally, the level of authorization control is limited, making them vulnerable to fraudulent activities.

If a customer sends a check via postal mail, there is always a possibility of it being intercepted, lost, or stolen during processing and delivery. This increases the risk of financial losses and can potentially harm the trust and confidence of both businesses and their customers. Implementing robust security measures to prevent check fraud, such as watermarking, magnetic ink, and other security features, can be costly and may still not provide foolproof protection.

Say goodbye to paper check headaches with Boost Payment Solutions

Simplify your reconciliation process and improve payment transparency by accepting commercial card payments with Boost Intercept, our patented straight-through processing technology.

- Save time and reduce risk by automating payment receipt, posting and remittance reporting

- Make informed decisions with actionable data and insights

- Receive enhanced remittance reporting options, including direct integration into treasury platforms

- Auto-reconcile card payments to the bank entry within AR systems through our customized reporting solutions.

- Accelerate DSO by reducing the time it takes to receive and deposit payments

- Protect your operations by eliminating unnecessary exposure to sensitive payment information

Ready to start accepting digital payments and increase cash flow? Contact Boost today.