Cash flow concerns put pressure on both sides of the trading relationship.

In an Atradius survey of businesses in western Europe, respondents said that economic conditions such as inflation and higher costs of funds were having a negative impact on them.

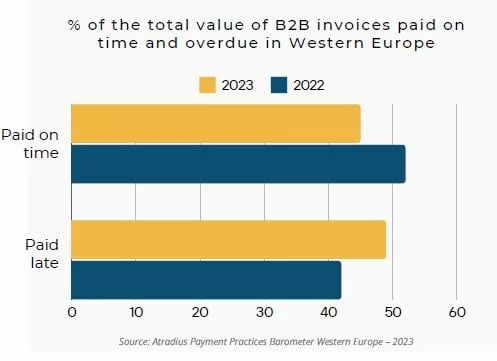

Many businesses reported finding it difficult to pay their bills at all. In fact, nearly half (49%) of the total value of B2B payments were paid late,

while only 45% were paid on time.

A separate survey by Intrum found that 37% of businesses in Europe pay their suppliers later than they would accept payments themselves. And more than half of European businesses said they would like to pay invoices faster but didn’t feel doing so was currently feasible.

Businesses are coping with this uncertainty by focusing on their working capital. This means that buyers are trying to extend their terms so they can keep their cash available longer. Suppliers, on the other hand, want to get paid as quickly as possible.

Against this economic backdrop, a case for increased commercial card usage is growing.

Historically, card use for B2B transactions in Europe has been limited, Stynen said.

Usage has been driven by buyers, who were looking to take advantage of rebates or trying to extend their payment terms. But because suppliers were footing the bill by paying card transaction fees, they were less likely to agree to accept cards.

Now, however, the case for card usage is expanding while some barriers decline.

A need for flexible cash flow solutions is emerging.

As businesses on both sides of the trading partnership respond to the economic uncertainty, they’re seeking better solutions. Globally, 94% of companies report taking some kind of action to minimize the impact of inflation on their businesses.

Rising interest rates have made loans more costly. Some suppliers are finding that accepting credit cards can be less expensive than bank loans and more flexible than other available solutions such as invoice factoring.

For their part, buyers are continuing to find the use of credit cards an effective way to get credit. To that end, they’re looking to increase card acceptance among their suppliers and are willing to help make it more attractive to them.

“Buyers looking to increase terms with their supplier base are offering card payment as a mitigating tool. So the supplier has a choice: accept a longer term, or accept cards at the same or reduced term,” Stynen said.

“Buyers are also looking to expand their DPO (days payable outstanding) using card payments. So they’re working out an arrangement with the supplier to offset part of the card fees.”

These sorts of arrangements are helping card payments to offer more benefits for both parties, Stynen said.

Legacy processes are giving way to improved technology.

Newer and nimbler payments partners have also started taking advantage of improved technology to automate and streamline previously clunky card-related processes.

In response to strict AML and KYC requirements, legacy providers had developed onboarding and underwriting procedures that are both time and labor-intensive. As a result, suppliers were often reluctant to jump through the hoops that were required to accept cards, Stynen said.

Newer entrants have found ways to meet requirements that keep the payments system safe and secure with processes that are faster and easier for suppliers. For example, companies like Boost can automate the payment process from beginning to end, a solution known as straight-through processing (STP).

STP has also emerged as an efficient way of dealing with B2B virtual card payments for suppliers that do not currently accept cards and those that want to cut out their operational involvement in card processing,” Stynen said.

STP providers sit between the buyer, the supplier and the financial institutions. Suppliers integrate their enterprise resource planning (ERP) software

with the STP provider’s platform.

Then, when a buyer pays an invoice with a virtual card, the provider pushes the funds along with the associated data and reporting to the supplier.